Conditions for NOW 3, changes to NOW 1 and 2 and opening NOW 1 Subsidy Determination Desk

In recent months the government has supported the business sector in various ways, including by means of two emergency packages containing, among other things, the Temporary emergency bridging measure to retain jobs (Tijdelijke noodmaatregel overbrugging voor werkbehoud) (NOW 1 and NOW 2). On August 28, 2020 the government presented the relief and recovery package for businesses and workers as a follow-up to the first two emergency packages. This package took effect on October 1, 2020. NOW 3 is part of this package. In this context, the Minister of Social Affairs and Employment informed the Lower House of Parliament on September 30, 2020 about the precise conditions of NOW 3, several changes to NOW 1 and NOW 2 and about the opening of the NOW 1 Subsidy Determination Desk. We briefly addresses these matters.

NOW 3

1. General

NOW 3 is aimed at providing longer certainty to employers about the compensation of payroll costs. NOW 3 therefore has a term of nine months, spread over three tranches of three months. Just like NOW 1 and NOW 2, the aim is to retain jobs as much as possible. Because the corona crisis is lasting longer than initially thought, NOW 3 offers employers time to adjust their business operations to the new reality, without the associated decline in the payroll automatically triggering a reduction of the subsidy amount.

2. An overview

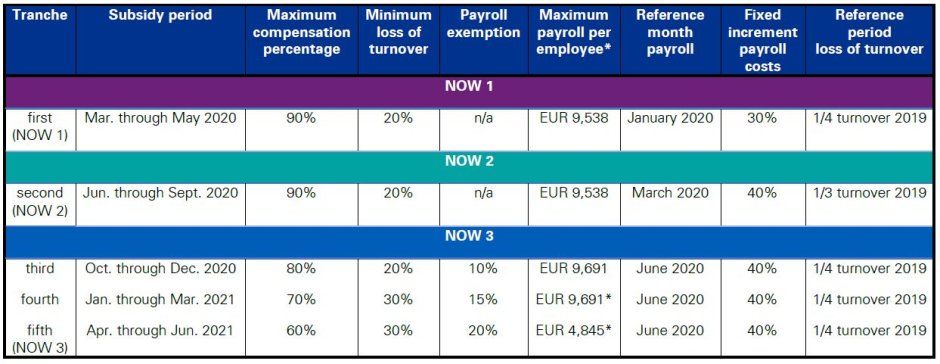

As clarification, the following table lists the most important features and parameters of NOW 1, 2 and 3.

* The maximum daily wage is indexed as of July 1, 2020 and therefore another amount applies to the third tranche than to the first and second tranches. As of January 1, 2021 indexation will again take place and those amounts are relevant for the amount in tranches four and five. The amounts currently entered there are thus indicative and based on the maximum daily wage per month as it applied as of July 1, 2020.

3. What will change?

The above table shows that, in comparison to NOW 1 and 2, several aspects of NOW 3 have been or will be changed. This involves the following changes:

- As of the third tranche, the maximum compensation percentage will be gradually phased out (from 80% to 70%, to 60%; is 90% under NOW 1 and 2);

- In the fourth and fifth tranches, the minimum loss of turnover to be eligible for the NOW will be increased to 30% (is 20% under NOW 1 and NOW 2 and the first tranche of NOW 3);

- In the fifth tranche the maximum salary per employee to be taken into account will be reduced to once the maximum daily wage per month. Because this amount is indexed every six months, the maximum daily wage per month is currently not known. As an indication, as of July 1, 2020 the maximum daily wage per month is EUR 4,845.47;

- The reference month for determining the payroll is, in principle, June 2020.

Changes compared to NOW 1 and NOW 2:

- The payroll exemption.

The payroll exemption means that the payroll during the subsidy period may be less than three times the payroll in the reference month (in principle June 2020), without this having consequences for the subsidy amount. The purpose of this exemption is to give businesses more time to restructure. The payroll exemption increases per tranche: from 10% in the third tranche to 15% and 20% in the fourth and fifth tranches respectively. - The consequences for redundancy on economic grounds will no longer apply.

Under NOW 2 the entire subsidy amount will be reduced by 5% if, in the event of large redundancy applications (20 or more employees), no agreement is reached with the respective trade unions, or in the absence thereof, another employee representation about the number of people who will lose their jobs out of necessity. This reduction is canceled under NOW 3. In addition, under NOW 3 redundancy on economic grounds will no longer mean that 150% (NOW 1) and 100% (NOW 2) of the payroll of the relevant employees for the entire subsidy period is deducted from the final subsidy amount.

- A reduction of 5% of the subsidy amount if businesses fail to comply with their best efforts obligation to help employees made redundant (on economic grounds) to find new employment.

Under NOW 3, the Dutch Employee Insurance Agency (Uitvoeringsinstituut Werknemersverzekeringen; UWV) will check whether an employer submitted an application for redundancy on economic grounds during the subsidy period and, if so, whether the employer contacted the UWV via the UWV NOW telephone help line. Failing to comply with these conditions will result in a 5% reduction on the entire subsidy amount.

4. What stays the same?

In essence NOW 3 is comparable to NOW 1 and 2, i.e. compensation for payroll costs that is based on the loss of turnover and the payroll, with the aim being to retain as many jobs as possible. The following matters are also comparable:

- A prohibition on the awarding of bonuses, distribution of dividends and redemption of own shares.

The distribution and redemption prohibition remains fully in force under NOW 3. In the first, second and third tranches this prohibition applies, in principle, to the year 2020. For the fourth and fifth tranches, this prohibition applies to the year 2021. We expect that in the case of a split financial year the prohibition will apply to the financial year (or financial years) in which the relevant subsidy period falls, such as is also the case in the first and second tranches. - Businesses can elect the turnover period and the reference turnover remains the same.

To determine the loss of turnover, the reference turnover should be compared to the turnover in the elected turnover period. This reference turnover is calculated by dividing the turnover for 2019 by four. Just as in NOW 1 and 2, employers may, in principle, choose the period over which the decline in turnover must be calculated, as long as the starting date is the first of the month and the chosen month falls within the relevant tranche. However, if the NOW subsidy is claimed in consecutive tranches, the chosen turnover periods must directly follow one another. For example, if an employer also used NOW 2, then the turnover period for the first period of NOW 3 (the third tranche) must follow the turnover period chosen for NOW 2. - Businesses receive an advance payment of 80% and this will be paid in three installments.

5. Some practical matters

A number of practical matters are listed below:

- The text of the NOW 3 scheme will be published mid-October.

- The application for the advance payment (subsidy provision) must be made per tranche. The UWV aims to use the following application periods:

|

Tranche |

Application period |

|

Third |

November 16, 2020 through December 13, 2020 |

|

Fourth |

February 15, 2021 through March 14, 2021 |

|

Fifth |

May 17, 2021 through June 13, 2021 |

- The advance payment of 80% will be paid in three installments. The decision deadline is 13 weeks. The aim is, however, to make the first advance payment within two to four weeks of receiving the complete application.

- The application for the final subsidy (determination of the final amount of the subsidy) must also be made per tranche, but it will be determined by the UWV in one go as of September 1, 2021. The application must be made within 24 weeks. A deadline of 38 weeks applies if an auditor's statement is required.

Changes to NOW 1 and NOW 2

The changes introduced on September 30 amended the following aspects of NOW 1 and NOW 2:

- Revision opportunity applications at operating company level.

In practice it appears that there are businesses that have submitted a NOW application without realizing they are part of a group. To avoid that in such cases businesses cannot or can no longer claim the NOW scheme, NOW 1 and 2 have been amended. In short, it is now arranged that at the time the application for determining the final subsidy is submitted, employers may request that the subsidy be determined at the operating company level, whereby only at that time do they have to meet the conditions stipulated for a NOW application at the operating company level (instead of at the time of the application for the subsidy provision). - The dividend and bonus prohibition has been clarified.

The dividend and bonus prohibition applies to the year 2020. Awarding a bonus or distributing a dividend for the year 2020 after the financial statements have been approved is thus also contrary to the objective of the scheme. In the text of the NOW 1 and 2 schemes, the sentence “through to the date of the meeting in which the financial statements are approved in 2021”, which was originally intended as clarification, has therefore been deleted. - The obligation to send documents as proof of the decline in turnover has been removed.

Documents serving as proof of the reported decline in turnover and complying with the conditions attached to an application at the operating company level no longer have to accompany the application for the determination of the final subsidy amount. Both types of documents may of course be requested during an audit. - The end date of the NOW 1 scheme has been changed to August 1, 2022, in connection with the (in part previously) altered application and decision deadlines.

Determination of the final subsidy amount NOW 1

As of October 7, 2020 an application for the final subsidy (determination of the final subsidy amount) may be submitted. An employer has 24 weeks to do so. This period is 38 weeks if an employer has to provide an auditor’s statement. The UWV has 52 weeks to decide on the application, but aims to provide a definite answer by the end of November if possible.

If the determination of the final subsidy amount means that an employer has to repay some of the subsidy, a payment deadline of six weeks applies for this. It can request a payment arrangement within this period. The UWV will deal favorably with these requests and will generally offer businesses a payment arrangement of 12 monthly installments. If this payment arrangement also fails to provide relief, the UWV, together with the employer, will look for a customized solution.

Auditor’s statement

An auditor's statement is required if an employer has received an advance payment of at least EUR 100,000, the final subsidy amount is at least EUR 125,000 or if it submits an application at the operating company level. The protocol on the auditor’s statement(s) was published on September 11. In finalizing the protocol, consideration was given to finding a balance between customized solutions and careful examination on the one hand, and standardization and limitation of the administrative burden on the other.

Third party statement

A third party statement is required if an employer has received an advance payment of at least EUR 20,000 or the final subsidy amount is at least EUR 25,000. The activities of the expert third party mainly cover the established decline in turnover and the payroll. A comprehensive meeting with the management of the organization is mandatory. What is also relevant is that a business must provide full access to its accounts and records for 2019 and 2020. The expert third party must document their activities and account for them upon request. If mistakes or deviations are found, businesses are obliged to correct these in their applications.

The statement, with explanatory notes, can be accessed here.