As of January 1, 2019: new VAT rules for vouchers, stamps and tokens

As of January 1, 2019 new VAT rules apply to vouchers, stamps and tokens. The new rules are a result of the EU Voucher Directive, which is designed to harmonize the VAT treatment of vouchers within the EU. Until recently, there were no specific rules for the VAT treatment of vouchers in the Netherlands and other EU Member States. This meant that double taxation or double non-taxation arose in cross-border situations. The new rules must ensure that these situations become less frequent. We address some aspects of the new rules.

1. SPV and MPV

1.1 Distinction between SPV and MPV

A voucher is an instrument (in paper or electronic form) that can be redeemed or used as a (partial) consideration for the supply of goods and services. The goods or services to be supplied, or the identity of the potential providers thereof, and the conditions for use are stated on the voucher or in the accompanying documentation (such as the general terms and conditions).

The new rules distinguish between single purpose vouchers (“SPVs”) and multiple purpose vouchers (“MPVs”). In the case of an SPV, the place of supply of the good or the service and the VAT amount are known at the time the voucher is issued or transferred. In the case of an MPV, at least one of these two elements is still unknown.

Each transfer of an SPV by an entrepreneur acting in its own name and for its own account is regarded as a supply of a good or a service that is subject to VAT. The transfer of an MPV is not subject to VAT.

The qualification as SPV or MPV is important to, for example, determine when and by whom the VAT is due.

1.2 VAT liability in respect of SPVs

VAT on SPVs is due at the time these are issued or transferred. Under the old rules (before 2019) in the Netherlands, the issue of a gift card (as a payment instrument) was VAT exempt. VAT was only due when the consumer redeemed the gift card. If the gift card qualifies as an SPV under the new rules, then – unlike under the old rules – VAT will be due upon issue or transfer.

1.3 VAT liability in respect of MPVs

VAT on MPVs is only due at the time goods are actually exchanged or services are actually provided. An entrepreneur that, at the time of issuing or transferring their vouchers, does not want to be liable for VAT under the new rules, will have to press for having their vouchers qualified as MPVs. For example, a voucher with which both goods or services can be obtained at the reduced (9%) and the general VAT rate (21%). In these cases, the precise VAT treatment cannot yet be established upon issue or transfer.

1.4 Scope

The new rules apply to vouchers issued after December 31, 2018. The old rules still apply to vouchers issued before January 1, 2019. However, it is not easy for entrepreneurs to maintain two systems. That is why the Deputy Minister of Finance has provided for approvals in the Policy Statement dated December 14, 2018, as published on December 21, 2018. These approvals are addressed below in sections 3.1 and 3.2.

2. Free-of-charge vouchers

The Policy Statement specifically pays attention to free-of-charge vouchers (‘free vouchers’). These vouchers do not have to be paid for but are provided, for example, along with other supplies of goods or services, such as a voucher for ‘free’ towels when buying motor fuel. According to the Deputy Minister, what the consumer pays must be fully attributed to the motor fuel, the purchase of which is accompanied by a voucher. The Deputy Minister is of the view that this means that the voucher is provided ‘free of charge’.

Free vouchers can also be issued without another good or service being purchased. The Deputy Minister considers that the charging of VAT on free vouchers must be in line with the VAT treatment of goods and services provided for free.

2.1 Free vouchers for goods

According to the Deputy Minister, the provision of a free SPV for a good triggers a deemed supply of that good at the time it is provided. He also believes that redeeming a free MPV for a good triggers a deemed supply at the time the MPV is redeemed or used. In these cases, the following conditions must however be met:

- a full or partial VAT recovery right is applied; and

- the voucher can be redeemed for a good worth more than EUR 15.

We believe that this amount can be assumed to be EUR 15 excluding VAT. Moreover, this value, as described in the Policy Statement, must be assessed on the basis of the good for which the voucher is redeemed. This avoids the situation where the value per instrument (such as a loyalty point) represents the value if these instruments together form a voucher (such as in the case of a full loyalty card).

In the case of a deemed supply, the taxable amount is set at the purchase price of the goods or similar goods. If there is no purchase price, the cost price must be used, calculated at the time of the deemed supply.

2.2 Free vouchers for services

Unlike free vouchers for goods, a free voucher for a service does not trigger a deemed service. The Deputy Minister considers that this must be regarded as having been provided for business purposes and that there is thus no deemed service. According to the Deputy Minister, the transfer of such a voucher is a non-taxable transaction, which in principle leads to a limitation of the entrepreneur’s VAT recovery right.

2.3 Uncertainty about free vouchers

The VAT treatment of free vouchers as prescribed in the Policy Statement leads to considerable uncertainty. The distinction made in the VAT treatment of free vouchers for goods and services is in our view incomprehensible. It is highly questionable whether the Deputy Minister’s position on this point is in accordance with EU legislation and regulations.

Furthermore, in many voucher/business models the issuer of the voucher is a different entrepreneur to the party that actually supplies the goods or provides the services. The party that actually supplies the goods or services will often be able to redeem the surrendered voucher from the issuer of the voucher and receive a cash payment for it. In that case we believe that it cannot be argued that the supplier or service provider provides the goods or services for free and that the issuer pays the redeemed voucher. The Policy Statement appears to ignore this and only looks at the relationship between the issuer and the consumer.

It is strange that the VAT Deduction Exclusion Decree (Besluit uitsluiting aftrek omzetbelasting; hereinafter: “DED”) is not mentioned in the Policy Statement. Article 16a of the VAT Act 1968 prioritizes the DED above the deemed supply. We believe that where an entrepreneur issues an MPV to an existing customer, which the customer later redeems from the entrepreneur for a good, the provision of the good falls under the DED (with a threshold for VAT recovery purposes of EUR 227 excluding VAT, per customer per year), which makes a VAT correction unnecessary in many cases.

3. Transitional rules

As discussed in section 1.4, the Deputy Minister granted approval for transitional rules for SPVs and MPVs in the Policy Statement dated December 14, 2018. These may be used, but are not compulsory.

3.1 Transitional rules for SPVs

The Policy Statement contains an approval for entrepreneurs that issued SPVs which were still unredeemed or were not entirely used before January 1, 2019, to pay VAT as if the SPVs were issued on January 1, 2019. Insofar as these SPVs are not redeemed or used, the charging of VAT will continue to be disregarded under the approval and in line with the old rules. To be eligible for this approval, entrepreneurs must comply with several conditions. The entrepreneur that issued the vouchers must:

- apply the (other) new VAT voucher rules to the relevant SPVs;

- apply the VAT rate applying on January 1, 2019;

- not mention the VAT on their invoices;

- report the VAT in their VAT return for the first period of 2019;

- base the percentage of non-redeemed vouchers on the average of the objective historic data of the last three years;

- inform the entrepreneurs where their vouchers are redeemed or used about the application of this approval.

3.2 Transitional rules for MPVs

The Policy Statement also provides a similar approval for MPVs. The Deputy Minister has approved that MPVs that were issued before January 1, 2019, but not yet redeemed or used on that date, may be treated as if these were issued on January 1, 2019. The entrepreneur that issued the vouchers must:

- apply the new VAT voucher rules to the relevant MPVs;

- apply the VAT rate applying at the time the vouchers are redeemed or used; and

- inform the entrepreneurs where the vouchers are redeemed or used about the application of this approval.

Because under the old rules VAT was also only payable at the time the voucher was redeemed for a product, this approval does not affect the time when VAT becomes due. The approval may however affect the taxable amount or the presence of distribution or promotional services.

4. Tokens, stamps and coupons

Under the new rules, tokens, stamps and coupons are not vouchers. The Policy Statement elaborates on the various characteristics of these instruments. These characteristics are briefly explained below.

4.1 Tokens

A token must be provided with a supply of a good or service and does not entitle the holder to cash but to a discount. The redemption of the token therefore always necessitates an additional payment. It can be inferred from the new rules that free tokens, accompanying the purchase of products, fall outside the scope of VAT. VAT is only due on the additional amount paid when redeeming the token for a good or service. If the tokens had to be paid for, then VAT must be paid upon redemption on the amount paid for the tokens and on any additional payment.

4.2 Stamps

A stamp is an instrument provided free of charge with goods or services that, whether or not together with other stamps, only entitles the holder to cash. A stamp does not entitle the holder to a discount or (part of) a product. The stamp rules apply to stamps. These rules have been tightened for the purposes of defining the stamp and voucher concepts. Under the stamp rules the difference between the VAT rates for the goods or services with which the stamps were issued (the issuance of stamps) and for the gift for which the stamps were redeemed (upon redemption of the stamps) is corrected. Entrepreneurs can request a VAT refund for the difference. Where the instrument still qualified as a stamp under the rules applying before January 1, 2019, but as of January 1, 2019 qualifies as a voucher, entrepreneurs will no longer be eligible for such a correction under the new rules.

4.3 Coupons

Coupons are instruments that provide an entitlement to a discount and are not provided with a supply of a good or service. Using coupons necessitates additional payment. According to the judgment rendered in the Granton Advertising BV case, VAT is due on coupons that are issued in exchange for payment. As stated in the Policy Statement, determining the VAT implications of the redemption of coupons depends on which entrepreneur bears the discount. This can be the entrepreneur where the coupon is redeemed, but it can also be the manufacturer or central body that bears the discount.

5. In summary

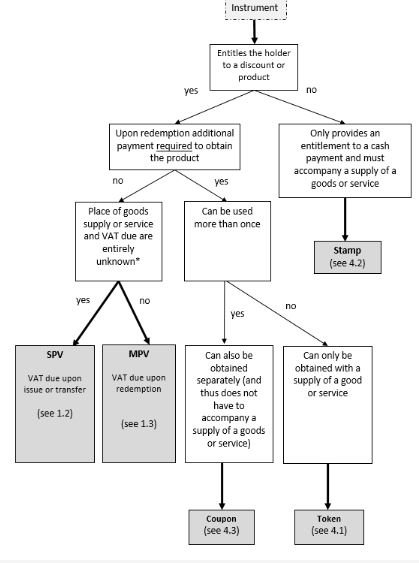

We have discussed the VAT treatment of vouchers (SPVs and MPVs) and in particular the free-of-charge vouchers. Coupons, tokens and stamps were also addressed. The following flowchart presents our understanding of the various instruments.

* is not the case if it is still unknown what the implications will be of a special tax scheme (such as the margin scheme or the Tour Operators Margin Scheme), if applicable.

6. Final remarks

Due to the very short time between publication of the Policy Statement and the date on which the new VAT voucher rules took effect, many entrepreneurs have still not been able to assess the exact consequences for their business. For entrepreneurs that have actively prepared for this, the new VAT voucher rules are also still rather ambiguous. They will want to obtain clarity in the coming period about the interpretation of the new rules or will want to adjust their model.

If your business is involved with the issue, transfer or redemption of vouchers, it is advisable to examine how the new rules will impact your business. Our VAT specialists in the Indirect Tax Group would be happy to help you with this.